Understanding financial statements can feel overwhelming if you’re not a finance professional, but knowing how to spot red flags is essential—especially if you’re an investor, business owner, or just someone looking to protect their money. Fortunately, you don’t need a degree in accounting to identify potential warning signs. By focusing on a few key areas, you can quickly assess whether a company’s financial health is as solid as it seems.

1. Inconsistent Revenue Trends

Revenue should follow a logical pattern based on the company’s industry and market conditions. If you notice sharp fluctuations without a clear reason, such as seasonality or a major event, it could signal manipulation or unreliable earnings. Look for:

Unusual spikes or dips not explained in the financial statements.

Inconsistent revenue recognition (e.g., recognizing revenue before delivering products or services).

A sudden surge in revenue near the end of a reporting period, which could indicate aggressive accounting practices.

2. Unexplained Expenses and Rising Costs

Pay close attention to expenses, especially if they are growing disproportionately to revenue. Red flags include:

High administrative costs that don’t match the company’s size.

Unexplained one-time charges that appear frequently.

Sudden changes in depreciation methods, which could be used to manipulate earnings.

3. Declining or Negative Cash Flow

Profit on paper doesn’t always translate to actual cash in the bank. A company may report profits but struggle with cash flow. Look for:

Operating cash flow that is consistently lower than net income, which could indicate accounting gimmicks.

Frequent reliance on financing (debt or issuing stock) to cover expenses.

Delays in accounts receivable payments, suggesting customers are struggling to pay.

4. Unusual Debt Levels

While debt is normal for businesses, excessive or rapidly increasing debt can be a warning sign. Check for:

A rising debt-to-equity ratio, indicating the company is relying too much on borrowed money.

Short-term debt that keeps rolling over, which may signal liquidity issues.

Interest payments consuming a large portion of earnings, reducing profitability.

5. Frequent Restatements of Financials

Companies occasionally revise financial statements due to errors or changes in accounting policies. However, frequent restatements can indicate poor financial controls or even fraud. Watch for:

Revisions that significantly change past earnings reports.

A history of accounting errors or regulatory investigations.

Discrepancies between reported earnings and tax filings.

6. Growing Inventory or Accounts Receivable

A company’s inventory and accounts receivable should align with its revenue growth. Red flags include:

A sharp rise in inventory without a corresponding increase in sales, possibly indicating overproduction or unsold stock.

Accounts receivable growing faster than revenue, which could mean the company is struggling to collect payments.

7. Opaque or Vague Disclosures

A company’s financial statements should be transparent and provide clear explanations for any major changes. Be wary of:

Overly complex language or missing key details in footnotes.

Frequent changes in accounting methods without clear justification.

Large off-balance-sheet liabilities, such as undisclosed leases or pension obligations.

8. Management Red Flags

Sometimes, the biggest warning signs come from leadership behavior rather than the numbers themselves. Look for:

Executives selling large amounts of stock, which could indicate a lack of confidence in the company’s future.

High turnover in the finance or executive team.

Legal or regulatory issues involving key personnel.

Final Thoughts

You don’t need to be a finance expert to spot potential red flags in financial statements. By focusing on revenue consistency, expense trends, cash flow, debt levels, and management behavior, you can get a clearer picture of a company’s financial health. If something looks off, don’t ignore it—dig deeper, consult a professional, or consider it a sign to proceed with caution. In the world of finance, being proactive is always better than being caught off guard.

In today’s competitive business world, financial stability is crucial for long-term success. Many businesses fail due to financial distress that could have been anticipated and prevented with the right tools. One such tool is the Altman Z-Score, a powerful metric that predicts the likelihood of bankruptcy. Developed by economist Edward Altman in 1968, this formula has become a widely used financial indicator among business owners, investors, and analysts. Understanding the Altman Z-Score can help you take proactive steps to safeguard your company’s future.

1️⃣ What is the Altman Z-Score?

The Altman Z-Score is a formula designed to assess a company’s financial health by analyzing key financial ratios. It measures a company’s ability to withstand financial distress by evaluating profitability, liquidity, leverage, and efficiency.

The standard Altman Z-Score formula for publicly traded manufacturing companies is:

Where:

X₁ = Working Capital / Total Assets (Liquidity)

X₂ = Retained Earnings / Total Assets (Profitability over time)

X₃ = EBIT / Total Assets (Earnings strength)

X₄ = Market Value of Equity / Total Liabilities (Leverage)

X₅ = Sales / Total Assets (Asset efficiency)

Different variations of this formula exist for private companies and non-manufacturing firms, making it a versatile tool across industries.

2️⃣ How the Z-Score Works

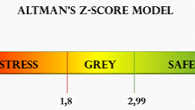

The Altman Z-Score categorizes businesses into three financial zones:

Safe Zone (Z > 2.99): The company is financially stable and has a low risk of bankruptcy.

Grey Zone (1.81 < Z < 2.99): The company is in a moderate risk category and requires financial improvements.

Distress Zone (Z < 1.81): The company is at high risk of bankruptcy and immediate corrective actions are needed.

By calculating and monitoring your Z-Score, you can identify early warning signs of financial trouble and take proactive measures to improve stability.

3️⃣ Why It Matters for Your Business

The Altman Z-Score serves as a financial early warning system, helping business owners and investors make informed decisions. Here’s why it matters:

Early Bankruptcy Detection: The Z-Score provides an objective measure of financial risk, allowing companies to address problems before they become critical.

Investor Confidence: A strong Z-Score can enhance investor and creditor confidence, making it easier to secure funding.

Better Financial Planning: Businesses can use the Z-Score to monitor their financial health and implement necessary changes to maintain stability.

Competitive Advantage: Companies that manage financial risk effectively have a strategic advantage over competitors who fail to monitor their financial indicators.

4️⃣ How to Calculate & Interpret Your Score

To calculate your company’s Altman Z-Score, you need accurate financial data from your balance sheet and income statement. Follow these steps:

Gather Data: Extract the relevant financial figures (working capital, retained earnings, EBIT, market value of equity, total liabilities, sales, and total assets).

Apply the Formula: Plug the values into the Z-Score equation.

Interpret the Results: Compare your score with the benchmark categories (Safe, Grey, or Distress Zone).

Take Action: If your company falls into the Grey or Distress Zone, develop strategies to improve financial stability.

5️⃣ Proactive Steps to Improve Your Score

If your business has a low Altman Z-Score, don’t panic. There are several steps you can take to strengthen your financial position:

Improve Liquidity: Maintain a healthy level of working capital by managing cash flow effectively and reducing unnecessary expenses.

Enhance Profitability: Focus on increasing revenue streams and reducing operational inefficiencies.

Optimize Debt Management: Lower excessive liabilities by restructuring debt and negotiating better loan terms.

Boost Asset Utilization: Ensure that company assets are being used efficiently to generate sales and income.

Monitor Financial Performance Regularly: Keep track of your Z-Score over time and adjust your business strategies accordingly.

Conclusion

The Altman Z-Score is a powerful tool that can help businesses predict financial distress before it’s too late. By understanding and applying this financial metric, you can protect your company from unexpected bankruptcy, secure investor confidence, and develop a more sustainable business strategy. Whether you’re a startup, a growing business, or an established company, regularly monitoring your Altman Z-Score can provide valuable insights and help ensure long-term success.

Start tracking your Z-Score today—it could be the key to saving your business!

Money isn’t just paper, numbers on a screen, or a means to pay bills. It’s energy. It moves, flows, expands, and contracts, just like any other force in nature. In fact, the very word currency comes from the Latin currere, meaning “to run” or “to flow.” When we recognize money as a dynamic force rather than a fixed resource, we can transform how we earn, spend, and invest—not just for financial success, but for a life of greater purpose and fulfillment.

Money as Energy: A New Perspective

Think of money as water in a river. When it flows smoothly, it nourishes everything in its path, supporting life and growth. But when it stagnates, it becomes murky and unusable. If it rushes too fast, it erodes everything around it. Money works the same way.

Many of us were raised with conflicting messages about money—either to fear scarcity or to chase more without clear purpose. But when we see money as a form of energy, it becomes something to be managed with intention, rather than something that controls us.

Like all forms of energy, money follows certain principles:

It is a medium of exchange – Money has no intrinsic value; it only gains power through how we use it.

It reflects our intentions – Where our money goes shows what we truly value.

It must be directed wisely – Just as energy can be wasted, stored, or used productively, money needs mindful management.

It responds to flow – Money is meant to move, not stagnate. The healthiest financial habits involve both giving and receiving.

Directing the Flow: How to Use Money Consciously

1. Clear the Blocks: Let Go of Scarcity Thinking

Many people experience emotional friction around money—whether it’s fear of not having enough, guilt over spending, or stress over making financial decisions. This mental clutter acts like a dam, restricting the natural flow of wealth.

Start by identifying limiting beliefs: Do you see money as something you must hoard? Do you feel undeserving of financial success? Awareness is the first step toward shifting these patterns. Money is simply a tool, neither good nor bad—it’s how we direct it that matters.

2. Align Money with Your Values

Because money is energy, where it flows reveals what we prioritize. Do your spending habits reflect what truly matters to you? If financial choices are made unconsciously, money often leaks into things that don’t bring long-term satisfaction.

A practical exercise: Look at your last month’s spending. Does it align with your highest goals and values? If not, adjust the flow—channel more of your money into experiences, investments, or causes that enrich your life.

3. Cultivate Balanced Circulation

Financial health isn’t just about accumulating wealth; it’s about how effectively money moves through your life. There are four key areas of flow:

Earning – Money coming in should be a reflection of your skills, effort, and contribution to the world.

Saving & Investing – This is like building reservoirs to sustain future growth.

Spending – Every dollar spent is a transfer of energy. Spend with awareness and purpose.

Giving – Just as nature thrives on cycles of giving and receiving, generosity keeps money energy vibrant.

Rather than seeing money as something to cling to or let slip away, aim for a rhythm that supports both security and expansion.

4. Remove the Resistance: Stop Fighting Your Money Flow

Have you ever noticed that when you stress about money, it seems harder to manage? Fear creates resistance, making it difficult to make sound financial decisions. When we trust that money flows and that we are active participants in its movement, we shift from a place of anxiety to empowerment.

Instead of fixating on lack or struggle, ask:

How can I create more value in the world?

How can I make financial decisions that bring ease and clarity?

Where can I redirect money flow for greater impact?

These shifts in mindset can transform financial challenges into opportunities.

5. Trust the Flow and Expand Prosperity

Just as a river nourishes everything it touches, money, when directed wisely, supports growth—not just for yourself, but for your community and the world. Wealth isn’t just measured in numbers; it’s measured in the opportunities, freedom, and well-being it creates.

The healthiest financial mindset is one of trust: trust in your ability to generate income, trust in your capacity to make wise choices, and trust in the natural circulation of wealth. When money flows in alignment with your values and purpose, prosperity follows—not just in bank accounts, but in every aspect of life.

Final Thought: Money as a Force for Good

By understanding money as energy, we move beyond financial stress and step into financial empowerment. It’s no longer just about accumulating wealth—it’s about mastering the flow. When money moves in alignment with our values, it becomes a powerful tool for creating a meaningful and abundant life.

The question is: Are you directing your money’s energy, or is it directing you?

Helping Executive Women Reduce Stress, Prevent Fatigue & Avoid Burnout 📩 Follow me for more insights or send me a message to connect!

When we travel overseas, we regularly find ourselves taking note and appreciating those subtle reminders of home.

Strolling past an RM Williams store in London, coming across our renowned surf or health brands in retail outlets, a famous Australian on the world sporting stage, or familiar brands of food and wine products in supermarkets.

Yet, there’s one major Australian export that is increasingly everywhere, but goes almost unnoticed, and that’s your super savings.

But make no mistake, as your super fund scours the world looking for opportunities to grow your retirement savings: it’s also strengthening not only Australia’s economic and diplomatic ties, but shoring up our growing influence on the international financial landscape as well.

While much of this flows into financial markets with investment in companies, it’s also being invested into ‘real’ assets.

So next time you find yourself in an airport in Vienna or Manchester, driving on a toll road in Italy, the USA or France, using the high-speed internet in regional Germany or spellbound by the magic of AI in the US, home might be closer than first thought. Indeed, there’s a pretty good chance you might even own a piece of these assets yourselves.

That’s the power of super – it gives working people a chance to gain exposure to multi-billion-dollar infrastructure investments that would otherwise not be possible. It lets hardworking Australians invest and own assets as though they’re the wealthiest people in the world.

This is a trend that will only continue as the Australian superannuation system expands – so much so, that capital itself will, in fact, become one of Australia’s most important exports. For a country renowned for its exports, that’s no mean feat.

The numbers speak for themselves – and they’re getting bigger and bigger. As of September, this year, the total pool of Aussies’ retirement savings is $4.1 trillion, or around 149 per cent of GDP – one of the largest pools of retirement capital in the world as a percentage of GDP.

By 2040, this pool of capital is expected to reach around $11 trillion or 193 per cent. Of this, the ‘institutional’ funds (industry, retail and government) account for $2.8 trillion currently, and this is expected to get to just over $8 trillion.

This capital is truly going global.

Institutional funds currently have around $1.2 trillion in offshore investments – or around 46 per cent of their invested assets.

If this proportion holds, the current quantum will need to treble to around $3.6 trillion invested overseas by 2040.

It is likely that this asset allocation will edge upwards somewhat as the Australian economy and the investment opportunities it presents simply won’t grow fast enough to absorb this. To put this task in context, the additional $2.4 trillion that will flow offshore is around 63 per cent of the just under $4 trillion Australia invests in total in overseas assets currently.

Where will it all go? Australian capital will clearly go to all corners of the globe, diversifying across global financial markets and real assets.

The housing market is not friendly to would-be buyers without help from mum and dad. So many are turning to the sharemarket for help.

Sophie MacPherson, 25, has been investing since she picked up a copy of The Barefoot Investor as a teenager and thought she ought to “dip a toe in”.

After eight years, she plans to use some of it for a home deposit.

MacPherson, who is a policy officer in Sydney, is among the growing number of young people turning to the sharemarket to turbocharge their savings in the hope they will make enough for a house deposit.

The combination of (until recently) lacklustre wage growth, higher rents and soaring home values make keeping up with property price growth a Sisyphean task for those trying to break into the market.

MacPherson was investing monthly into exchange-traded funds in 2022. Although she has stepped it back recently to chase high interest in her savings account, she still has about 50 per cent of her money in shares.

“Ideally, I wouldn’t liquidate my entire portfolio to buy a property, but I would liquidate some to help form a deposit,” MacPherson says, admitting it’s tricky to manage her HECS debt while breaking into Sydney’s “crazy” property market. So, she thinks it’s likely she’ll have to tap her investments.

“If the right property came up towards the end of this year or next year, we would definitely be open to putting an offer on something like that.”

Here is a guide to investing if you want to buy a property within one year, a couple of years or in a decade’s time.

Within a year

This timeframe is too short for investing in financial markets, says Melody Edwards, a financial adviser at Evalesco.

“The chance of losing capital over that amount of time is considerable,” she says. “So unless you’re flexible on your purchase date, to the extent you can ride through something happening, you really want to keep it more secure savings.”

HSBC head of investments Donahue D’Souza agrees that the amount of risk you can take on is tied closely to your timeframe.

“An investment horizon of up to two years is typically seen as short term, medium term is three to five and long term is greater than five years.”

A one-year timeframe is very short for the sharemarket, so if you’re planning to buy soon, cash is your friend, D’Souza says.

But that doesn’t mean you can’t make your money work hard.

Canstar analysis finds a person with $100,000 who put it into a high-interest saving account earning 5 per cent, and deposited $1000 a month, would earn $5018 in interest in 2025.

Someone with a $150,000 savings balance would reach $169,401 over the same period if they contributed the same $1000 a month, while someone with $200,000 would have $221,784.

The First Home Super Saver Scheme, in which borrowers can withdraw up to $50,000 of voluntary superannuation contributions, is another option and offers some tax benefits, as savings within super are taxed at only 15 per cent.

In two to three years

If you’re thinking of buying within two years, you’d still be largely in high-interest savings accounts, says Edwards.

But once you reach three years, you may consider adding a small portion of investments, such as diversified or exchange-traded funds. “You’d probably still be 75 per cent to 80 per cent in cash,” she adds.

D’Souza agrees liquid and defensive assets – those that are less likely to lose value – should still be front-of-mind in this scenario.

“Typically, these types of investments would include high interest and bonus interest savings accounts, term deposits and government bonds, if prepared to collect coupon payments and hold to maturity,” he says.

In three to five years

You have a little more room to play here, but still not a lot.

“You’re probably opening up a bit more in terms of adding growth,” says Edwards. “With three to five years, you would start increasing the growth allocation towards 50 per cent, but you’d try to diversify it as much as possible.”

That is, you’re not putting it all into just Australian banking shares, or US tech shares.

“Especially if the amounts are smaller, in terms of the regular savings that you’re putting into your investments, the easiest way to diversify would be to track an index and that’s the most cost-effective as well. Something like [an ETF tracking the ASX or the S&P500] is something we’d look at, or a diversified growth ETF that might mix the different indices as well.”

For example, ETF providers such as Vanguard offer products based on risk tolerance. Vanguard’s diversified conservative index ETF is described as medium risk, with a three year-plus timeframe.

Its diversified balanced ETF is also medium risk, but has a timeframe of five years-plus.

Others, such as its diversified growth ETF are considered high to very-high risk, and so it recommends holding them for at least seven years.

In 10 years

It’s not uncommon for Edwards to meet clients who want to buy further than five years out, particularly if they want a house rather than a unit, or they have quite a specific property goal.

For that saver, the first step is building up a three- to six-month buffer of living expenses. This is because these savers will invest much more in growth assets, such as shares, which they don’t want to draw down upon for a long time.

“Once that buffer is built, it’s about deploying 70 to 80 per cent of their wealth into growth assets. The rest will be in cash or fixed income,” says Edwards.

Those growth investments will still be in broad ETFs or index funds.

You have a bit more time now, so you can afford to take more risk as you have longer for the market to recover, agrees D’Souza.

“This portfolio is mainly growth-oriented with increased exposure to equities, global equities, and thematic plays.

“Given the higher risk, investors will likely use active ETFs and leverage the expertise of a financial adviser or fund manager to actively manage and adjust the portfolio exposures to increase returns and actively manage the risk,” he says.

If you’ve got a 10-year timeframe, you may consider adding an element of leverage to your investment strategy.

ETF provider Betashares launched a suite of products this year called Wealth Builder ETFs. These products track an index and are leveraged at a range of 30 to 40 per cent, meaning that for every $100 invested, the investor is granted $143 to $167 worth of exposure to the related index.

Betashares says $10,000 invested in the ASX200 from September 2010 to March 2024 would have grown to $30,400, but if that same sum was leveraged at a loan-to-value ratio of 30 to 40 per cent, it would have grown to $37,400.

But, notes Edwards, any time you introduce gearing, you increase risk. “That would be something where you only put in as much as you are comfortable to lose, over that short-term period,” she says.

How do I split it?

It’s not a simple matter of transferring, say, half of your savings into ETFs in one fell swoop, says Edwards.

Instead, you need to figure out what you’re trying to achieve for your deposit and then work backwards.

She gives this example: “Let’s say the starting point is $50,000 and the target is $100,000 deposit and the timeframe is five years – to save the $50,000 you would need to put aside about $192 per week into a savings account.

“A way to potentially grow your savings would be to invest a portion of these funds, keeping sufficient funds as an emergency buffer. We typically target three to six months.

“If your annual living expenses are $60,000, keep $30,000 as your buffer and start your investment with $20,000 and then with your regular savings, direct 50 per cent to savings and 50 per cent into investments.”

If you’re starting with $100,000, and plan to invest a larger amount, say $70,000, she says it’s worth considering dollar cost averaging over four months (so $17,500 in each instalment) to minimise market timing risk.

“We would usually look at dollar cost averaging between three and six months depending on the amount invested and your comfort level. Usually, the more to invest, but less familiar with investments would take over a longer period.”

Although she’s used a five-year timeframe, she says this buyer would have to be comfortable extending their purchase date if markets were to drop and fail to recover within that span.

“The big question [for people trying to save a deposit is] what is the timeframe and what are you looking at to buy?” Edwards says.

“The answers to those questions will help guide us around what’s reasonable, and what might require a little bit more work.”

Consider topping up your super because – after reducing your mortgage – it’s the most tax-effective structure for your money. And super is not just for high-income earners. Low-income earners may receive a top-up from the government after tax time of up to $1000.

Concessional contributions

Pre-tax contributions (concessional contributions) provide the opportunity to grow your retirement savings while reaping tax benefits along the way.

While the greatest benefit goes to people earning $190,000 to $250,000, those earning up to $37,000 who derive at least 10 per cent of their income from employment or business receive a low-income super tax offset payment of up to $500. It effectively refunds the 15 per cent tax paid on their super contributions.

The concessional contributions cap is $30,000, up from $27,500 in 2023-24.

The superannuation guarantee (SG) rate increased to 11.5 per cent on July 1, 2024. So, the opportunity for wage earners to make increased voluntary pre-tax contributions during this financial year is partly absorbed by the increase in their employer’s compulsory contributions.

From July 1, 2025, the SG rate rises to 12 per cent.

If you’re aged 67 to 74 and wish to claim a tax deduction for a personal contribution, you must meet the work test – 40 hours of gainful employment in 30 days.

If you can’t meet this test, but met it in 2023-24 and had a total superannuation balance below $300,000 at June 30, 2024, then you may contribute under the “work test exemption” provided you haven’t used this exemption before.

Generally, you have until 28 days after the end of the month in which you turn 75 to contribute.

Catch-up concessional contributions

If you didn’t use the full $27,500 concessional contributions cap in each of the last three financial years (or the $25,000 cap in the two years before that), then any unused amounts may be contributed this year, giving you a bigger deduction and tax saving.

Do this by making a larger personal contribution and claiming it as a tax deduction, or increasing salary sacrifice contributions.

But the catch is your total superannuation balance must have been less than $500,000 at June 30, 2024.

Unused cap amounts can be carried forward for up to five years, so this financial year is the last year to use any unused amount from 2019-20 – use it or lose it.

For some people, it may mean a tax deduction of up to $162,500. And for SMSF members able to use what is called a contribution reserving strategy and make a double contribution in June 2025, it could be as high as $192,500.

Using unused cap amounts can be extremely useful where you need to make a large one-off contribution to reduce capital gains tax arising from, say, the sale of an investment property.

Non-concessional contributions

The non-concessional (after tax) contributions cap is $120,000.

Anyone under 75 – whether working or fully retired – can make an after-tax contribution provided their total superannuation balance was less than $1.9 million at June 30, 2024.

If you haven’t triggered the bring-forward rule in the last two financial years and were under 75 at July 1, 2024, you may contribute up to $360,000 provided your total superannuation balance was less than $1.66 million at June 30, 2024, and up to $240,000 if it was $1.66 million to less than $1.78 million.

So, check your contributions since July 1, 2022. Look out for any excess concessional contributions not withdrawn from super as they count as non-concessional contributions and may have caused you to inadvertently trigger the bring-forward rule – a trap for the unwary.

Downsizer contributions

From age 55, you may be eligible to make a downsizer contribution of up to $300,000 ($600,000 for a couple) where you sell a home that you or your spouse owned for at least 10 years and contribute the proceeds within 90 days of settlement.

A downsizer contribution allows you to boost your super even if you’re otherwise ineligible to contribute due to age or total superannuation balance – you can contribute even if you’re aged 75 or more or have $1.9 million or more in super.

Other contributions

If your income will be less than $45,400 with at least 10 per cent of it coming from employment or business, then consider contributing $1000 to get a $500 top-up from the government – free money. But you must be under 71.

The co-contribution progressively reduces where you earn between $45,400 and $60,400.

You could make a contribution for your spouse provided they’re under 75.

If your spouse earns less than $37,000 and you contribute up to $3000, you can claim an 18 per cent tax offset – a benefit of up to $540. The tax offset progressively reduces where they earn between $37,000 and $40,000.

Boosting your spouse’s super while getting a tax benefit in the process is a win-win situation.

If you’re an eligible small business owner selling your business or an active business asset, don’t overlook the opportunity to make a CGT cap contribution of up to $1.78 million.

And if you’re using super to save for your first home, a voluntary contribution of up to $15,000 will help you get to the maximum releasable amount of $50,000 under the First Home Super Saver Scheme quicker – it takes years to get the greatest benefit from the scheme.

Starting a super pension

If you’re looking to start your first pension, the limit on how much you can transfer into it – the general transfer balance cap – is $1.9 million.

On July 1, this cap may increase to $2 million depending on movements in the CPI – meaning you could get more into the tax-free retirement phase.

So, if you’re going to be limited by this cap (which also affects how much you can receive by way of a death benefit pension when a loved one dies), you may want to hold off starting a pension – other than a transition to retirement pension – until then.

If you started a pension before July 1, 2024, your transfer balance cap will be less. You can obtain it from ATO Online via myGov.

Should you require more income than the requisite minimum, consider taking it as a lump sum withdrawal – partial commutation – because it helps your transfer balance cap.

Now is an ideal time to plan to get ahead of the game before tax time in June, which will be upon us before you know it.

When we travel overseas, we regularly find ourselves taking note and appreciating those subtle reminders of home.

Strolling past an RM Williams store in London, coming across our renowned surf or health brands in retail outlets, a famous Australian on the world sporting stage, or familiar brands of food and wine products in supermarkets.

Yet, there’s one major Australian export that is increasingly everywhere, but goes almost unnoticed, and that’s your super savings.

But make no mistake, as your super fund scours the world looking for opportunities to grow your retirement savings: it’s also strengthening not only Australia’s economic and diplomatic ties, but shoring up our growing influence on the international financial landscape as well.

While much of this flows into financial markets with investment in companies, it’s also being invested into ‘real’ assets.

So next time you find yourself in an airport in Vienna or Manchester, driving on a toll road in Italy, the USA or France, using the high-speed internet in regional Germany or spellbound by the magic of AI in the US, home might be closer than first thought. Indeed, there’s a pretty good chance you might even own a piece of these assets yourselves.

That’s the power of super – it gives working people a chance to gain exposure to multi-billion-dollar infrastructure investments that would otherwise not be possible. It lets hardworking Australians invest and own assets as though they’re the wealthiest people in the world.

This is a trend that will only continue as the Australian superannuation system expands – so much so, that capital itself will, in fact, become one of Australia’s most important exports. For a country renowned for its exports, that’s no mean feat.

The numbers speak for themselves – and they’re getting bigger and bigger. As of September, this year, the total pool of Aussies’ retirement savings is $4.1 trillion, or around 149 per cent of GDP – one of the largest pools of retirement capital in the world as a percentage of GDP.

By 2040, this pool of capital is expected to reach around $11 trillion or 193 per cent. Of this, the ‘institutional’ funds (industry, retail and government) account for $2.8 trillion currently, and this is expected to get to just over $8 trillion.

This capital is truly going global.

Institutional funds currently have around $1.2 trillion in offshore investments – or around 46 per cent of their invested assets.

If this proportion holds, the current quantum will need to treble to around $3.6 trillion invested overseas by 2040.

It is likely that this asset allocation will edge upwards somewhat as the Australian economy and the investment opportunities it presents simply won’t grow fast enough to absorb this. To put this task in context, the additional $2.4 trillion that will flow offshore is around 63 per cent of the just under $4 trillion Australia invests in total in overseas assets currently.

Where will it all go? Australian capital will clearly go to all corners of the globe, diversifying across global financial markets and real assets.

That means taxing the assets that make up the super fund providing annual income to retirees before the assets are even sold.

It could force properties held in super to be sold as their value rises, which is making plenty of older Australians decidedly uncomfortable.

The tax hike laws are currently held up in the Senate and might not pass, but if they do we would be the first nation on earth to ever legislate such a whacky policy.

The growing concerns among retirees reminds me of the backlash Shorten faced ahead of his ill fated attempt to win the 2019 federal election by arguing the case for changes to franking credits.

That election was thought to be in the bag for Labor. Unloseable given all the leadership turmoil within the Coalition government, and given that Labor led in every major opinion poll published over the course of two years counting down to election day.

The turnaround on the day was put down to a backlash, especially amongst older Australians, because of policies like the franking credits changes.

Self funded retirees understandably crack it when they plan for their fixed income retirement based on tax structures that get changed, eroding their fixed income when they no longer have the capacity to work to supplement it.

Which is exactly what Labor’s doubling of the super tax will do, not to mention the assets in super funds that will need to be sold because of the plan to tax unrealised gains.

Property in super portfolios is one of the most ill-liquid asset classes going around.

Fancy having to sell a property in your super fund because some assessor says it’s notional value has increased over the previous year as house prices continue to soar – when living off the rent from that property was your retirement plan.

That’s the real world impact of Albo’s super changes, which by the way, weren’t even taken to the last election.

He told us before the 2022 election that if Labor was elected to government there would be no new taxes.

So the attempt to double the super tax is another broken election promise, if it gets legislated.

One that has the potential to hurt Albo electorally the same way Shorten’s proposed tax hikes hurt him at the 2019 election.

You can see the Coalition sharpening their attack ads as it prepares to try and oust Albo from office early next year.

While the Senate might save Albo and Labor from its planned broken election promise by rejecting the proposed legislation necessary to increase super taxes, I’m not sure that prevents a backlash at the ballot box.

We know Labor wanted to double super taxes. We know that if it gets re-elected it will try and legislate the tax hike in its second term.

So the foundations for a strong campaign to chuck Albo out lest he slugs self funded retirees with higher taxes if he wins a second term have already been laid.

Credit scores can be full of surprises! Here are some lesser-known facts about credit scores:

1. Multiple Scores Exist

You don’t have just one credit score. Different scoring models, like FICO and VantageScore, use distinct criteria, leading to variations in your score. Even within the same model, lenders may use tailored versions specific to their needs.

2. Soft Inquiries Don’t Impact Your Score

Checking your own credit report or applying for pre-qualified offers are considered “soft inquiries” and won’t hurt your score. Only “hard inquiries,” triggered by formal credit applications, might lower your score.

3. Utilization Matters More Than Total Debt

Credit utilization ratio (the percentage of available credit you’re using) heavily influences your score. Even if you have a low overall debt, maxing out a single credit card can hurt your score.

4. Closed Accounts Can Affect Your Score

Closing old credit accounts might reduce your score because it can lower your credit history length and available credit, affecting utilization ratios.

5. Medical Debt is Weighed Differently

Medical debt is often treated more leniently in scoring models. Some scores disregard paid medical collections entirely, and newer FICO models prioritize other debts over unpaid medical bills.

6. Utility and Rent Payments May Count

Traditionally, utility and rent payments didn’t factor into credit scores, but programs like Experian Boost and some VantageScore models now allow such data to improve your score.

7. Good Behavior Takes Time to Reflect

Improvements in paying off debt or reducing utilization may not reflect on your score immediately. Credit bureaus update their information monthly or less frequently.

8. The Myth of “Joint Credit Scores”

Credit scores are always individual. Even for joint accounts, each person has their own score, influenced by their credit behavior.

9. You Can Have a “Thin File”

If you lack enough credit history, you might have a thin credit file, making it harder to generate a score. This often happens to young adults or those who primarily use cash.

10. Having No Debt Doesn’t Guarantee a High Score

A good credit score requires a history of managing debt responsibly. Without any credit accounts, there’s little data for scoring models to evaluate.

11. Negative Information Fades Over Time

Most negative marks, like late payments or collections, drop off your report after 7 years. Bankruptcies may last longer, but their impact diminishes over time.

12. Your Income Doesn’t Affect Your Score

Credit scores are based on your credit history, not your income. However, lenders may consider income separately when evaluating creditworthiness.

13. Credit Scores May Affect More Than Loans

Employers, landlords, and insurance companies might use your credit report (but not your score) to assess risk or responsibility.

14. Overpaying Won’t Boost Your Score

Paying more than the minimum is great for reducing debt and avoiding interest, but it doesn’t provide extra credit score benefits beyond demonstrating on-time payments.

15. Authorized Users Can Benefit

Being an authorized user on someone else’s account can help you build credit, provided the primary account holder manages the account responsibly.

16. Old Debts Aren’t Automatically Removed

Paying off an old debt doesn’t remove it from your credit report—it just updates the status. Positive credit behavior takes time to overshadow past issues.

Here are five valuable benefits of knowing and consistently tracking your credit score:

Helps Secure Better Interest Rates A higher credit score can qualify you for lower interest rates on loans, credit cards, and mortgages. Knowing your score allows you to estimate what rates you may qualify for and gives you a chance to improve your score before applying, which can lead to significant savings over time.

Improves Chances of Approval for Credit and Loans Knowing your score gives you insight into your chances of approval for credit or loans. By understanding your score and working to improve it if necessary, you increase the likelihood of being approved, avoiding unnecessary hard inquiries from declined applications.

Boosts Financial Planning and Goal-Setting Monitoring your credit score helps keep you focused on responsible credit habits, which can be crucial in achieving financial goals. For example, knowing what affects your score can motivate you to pay down debt, make timely payments, and improve your overall financial health.

Reduces Risk of Identity Theft Regularly checking your credit report can alert you to unusual activities, like unauthorized accounts or hard inquiries, that might indicate identity theft. Catching these early can help you take action quickly, preventing further damage and potentially sparing you from financial losses.

Empowers Negotiation and Leverage With a high credit score, you’re in a better position to negotiate terms, from credit card limits to loan terms. Lenders are more likely to offer favorable conditions to those with strong credit, so tracking your score and knowing where you stand can give you leverage when negotiating rates and fees.